This source is a transcript from William Cooper’s radio program, “The Hour of the Time,” featuring audio from a 1999 seminar titled “The Legality of Taxes.” The text captures a series of presentations by pioneer researchers and former government agents who argue that the federal income tax is a fraudulent system lacking a valid legal foundation. Central to their thesis is the claim that the 16th Amendment was never properly ratified and that no existing law or regulation actually mandates that most citizens file tax returns. Individual speakers, such as Bill Benson and Joe Bannister, share personal accounts of uncovering corruption and resigning from state and federal agencies to expose what they describe as unconstitutional and treasonous practices. Ultimately, the text serves as a call to action for public education, urging listeners to research the law and challenge the government’s taxing authority through civil and legal resistance.

B.A.T.F. / IRS Criminal Fraud by William Cooper (CAJI News Service)

Other Episodes Concerning Taxes

![🎧IRS and the BATF⚖️ - Bill Cooper's The Hour of the Time [Ep. #728-729]](https://substackcdn.com/image/fetch/$s_!TIte!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-video.s3.amazonaws.com%2Fvideo_upload%2Fpost%2F203465600%2F356e50ad-3f29-4360-9e9a-ee6413010cf7%2Ftranscoded-1782337163.png)

The Student’s Guide to Legal Word Magic: A Terminology Primer on Tax Jurisdiction

Introduction: The Art of Legal Illusion

In the sophisticated study of legal linguistics, words are not merely vehicles for communication; they are the architecture of jurisdiction. The modern tax landscape is built upon a foundation of “Legal Magic”—a strategic application of language designed to facilitate a polysemic trap. In this framework, a single word carries a common meaning for the public while concealing a hidden, statutory meaning that binds the individual to specific obligations. This use of language is a primary tool of jurisdiction in maritime and contract law, intended to move the individual into a specific venue without their conscious consent.

For the new learner, deciphering these definitions is the fundamental difference between offering a voluntary tribute and fulfilling a lawful requirement. Without linguistic literacy, the “Citizen” is reduced to a “beast of burden,” accepting a status they do not legally hold.

Legal Magic Defined “Magic is the art of illusion—deception, if you will. Those who practice magic are called the Magi... They have created a web of obfuscation and confusion in the Law. When the courts have ruled them unconstitutional or unlawful, they have merely stepped outside jurisdiction and venue. By fooling the people, they continued the crime.”

This linguistic illusion is not merely auditory; it is fundamentally typographic. The foundation of jurisdiction often rests on the visual representation of names and entities on the printed page.

Deciphering Typography: The Significance of Capitalization

In the realm of legal word magic, the casing of a letter signals a jurisdictional shift across thousands of miles. Typography serves as a tool of contract; the use of all-capital letters or specific lowercase formatting distinguishes between the constitutional republic and offshore trust identities.

The “INTERNAL REVENUE SERVICE” in all capital letters represents a specific trust identity associated with “International Operations.” By utilizing these iterations interchangeably in the Federal Register and the U.S. Code, the government obscures the fact that the entity claiming authority is often an offshore identity rather than a domestic agency. Visual formatting acts as the mask, while the statutory definition of geography serves as the stage for the illusion.

Defining the “State” and the “United States”

To the uninitiated, a “state” is one of the fifty members of the Union. However, statutory construction in 26 CFR § 31.3121(e)-6 and 18 USC § 921 reveals a dual-track sovereignty. The federal government utilizes two terms that sound identical but occupy vastly different legal space.

The Geographic Distinction:

united States (lowercase ‘u’): Refers to the republic and the “several states” of the Union.

United States (uppercase ‘U’): Refers to the federal corporation, its specific properties, possessions, and the District of Columbia.

Entities Included in the Federal Statutory “State” (The Federal Zone):

The District of Columbia

The Commonwealth of Puerto Rico

The Virgin Islands

Guam

Northern Mariana Islands

Territories and Insular Possessions

By substituting “United States” for “united States” in legal documents, the federal government extends its jurisdiction into the fifty states where it lacks constitutional power to tax individuals directly. Most critically, the linguist identifies that the “U.S. Constitution” referenced in these tax venues is allegedly the Constitution of Puerto Rico, not the Constitution for the united States of America.

The Legal Status of the Individual: “Citizen” vs. “Person”

The distinction between common usage and statutory meaning is most deceptive regarding the status of the individual.

Citizen (Capital C): A “Citizen of a State” (e.g., California). These individuals are subject only to the 18 powers cited in the Constitution for the united States.

citizen (lowercase c): A “U.S. citizen.” Statutorily, this refers to a person residing in a federal possession (like Guam or D.C.) subject to the plenary power of Congress.

Common Meaning vs. Statutory Meaning

Individual

Common: Any human being.

Statutory: Specifically a resident or citizen of Guam or the U.S. Virgin Islands.

Employee

Common: One who works for a paycheck.

Statutory: An individual employed specifically by the federal government.

Resident

Common: Someone living in a specific locale.

Statutory: An alien citizen of a possession (like Puerto Rico) residing within one of the fifty states.

The “Person vs. Thing” Deception: A definitive instance of linguistic substitution is found in the Federal Register (Vol. 41, No. 180), which asserts that the term “Director of Alcohol, Tobacco, and Firearms Division”—a specific human person—was replaced by the term “Internal Revenue Service”—an organization or “thing.” This allows the IRS to operate legally as a single person. This transition was facilitated by Acting Secretary of the Treasury Charles E. Walker, who signed Treasury Order 120-01, effectively joining these entities into a single, obfuscated authority. Furthermore, Form 1040 is technically the return for non-resident alien citizens of the U.S. Virgin Islands; by signing it, a Citizen of a State effectively swears an affidavit that they hold this alien statutory status.

Agency Identity: Trusts vs. Government Departments

Evidence suggests the IRS and BATF are not agencies of the U.S. Treasury Department, but are instead offshore pure trusts. The Secretary of the Treasury acts as the Trustee, while also serving as the “U.S. Governor of the International Monetary Fund,” an agency of the United Nations from which he receives a salary.

(The following section is from my notes on Trusts: https://docs.urbanodyssey.xyz/ucc/trusts.html)

To maintain this impenetrable veil of secrecy and extract wealth without consequence, the architects of global finance exploit highly specific, weaponized legal loopholes:

The “Flee Clause” Directive

Offshore trusts are specifically armored with “flee clauses.” This contractual loophole legally obligates the trustees to instantly shift the trust’s location to another sovereign jurisdiction at the very first sign of civil unrest, war, or—most importantly—unwanted attention from law enforcement or tax authorities. This ensures the laundered capital remains perpetually out of reach, moving faster than any international warrant or subpoena.

The Anstalt Anonymity Shield

Pioneered in Liechtenstein, the anstalt is a unique corporate structure functioning as an anonymous, single-shareholder company or trust. Operating under the world’s tightest corporate secrecy laws, the anstalt loophole allows the ultimate beneficiary to remain entirely hidden. This specific structure has been utilized by the CIA, the KGB, global arms dealers, and Swiss bankers to launder stolen funds, finance covert coups, and safely stockpile the proceeds of white-collar crime.

Territorial Privacy and the Puerto Rico Loophole

The elite use offshore territorial jurisdictions to shield trust records from domestic scrutiny. A prime example is the Internal Revenue Service (IRS) itself, which operates technically as a trust domiciled in Puerto Rico. By exploiting the territorial domicile of the trust, the entity’s records are protected by specific local laws that guarantee the absolute privacy of trust records, making the money trail for trillions of dollars nearly impossible for the public to audit or follow.

The Constructive Trust and the “Straw Man”

Beyond offshore banking, the system exploits the “constructive trust”—a trust that arises not by voluntary agreement, but by operation of law and fraud. When a birth certificate is registered, the state constructs a cestui que trust, rendering the living human as the co-trustee saddled with all duties, tax liabilities, and obligations, while the corporate state extracts the benefits. In the commercial tribunals masquerading as courts, the judge acts merely as the executor of this constructive trust, dictating which corporate entity owes money without the living human ever realizing their biological property has been hypothecated.

Future-Tense Jurisdictional Void

At the microscopic legal level, trusts are drafted utilizing “future-tense” grammar to create a jurisdictional black hole. By placing property into a trust using future-tense language, the creators establish a fictional jurisdiction with “no-rules, no-constitution, no-country, no-money.” This grammatical loophole suspends the assets out of “now-time” reality, sheltering the property from current tax liabilities and ensuring the funds remain untouched until the elite are ready to harvest them.

Statutory Secrecy and Notice Waivers

Even within standardized domestic law, such as the Uniform Trust Code (UTC), loopholes are maintained to ensure absolute darkness. Legal provisions allow the terms of a trust to override the default rules of disclosure, permitting a trust to be kept totally secret from its beneficiaries. By waiving the requirement to notify beneficiaries, the trustee is rendered completely unaccountable, opening the door for systemic mismanagement, laundering, and the creation of “illusory” trusts designed solely to hide assets from creditors and the state.

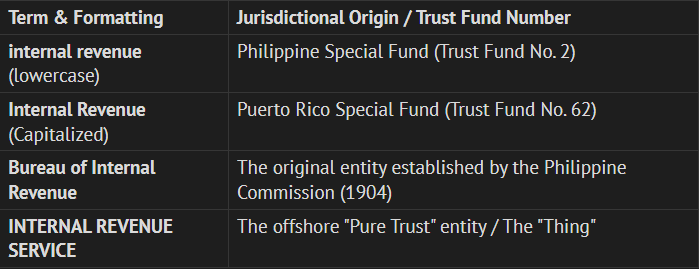

The Three Primary Offshore Trusts:

Philippine Trust #1: Philippine Special Fund (Customs Duties).

Philippine Trust #2: Philippine Special Fund (internal revenue—lowercase).

Puerto Rico Trust #62: Puerto Rico Special Fund (Internal Revenue—uppercase).

Legitimacy Checklist: Title 31, Chapter 3 of the U.S. Code provides the statutory list of all legitimate organizations within the Department of the Treasury. To be a legitimate branch of the government, an agency must meet the following:

Created by an Act of Congress: The IRS and BATF were created via Treasury Orders (e.g., 150-06 and 120-01), not by Congressional legislation.

Listed in Title 31, Section 3: Neither the IRS nor the BATF appear on this mandatory statutory list.

Possess Franking Privileges: Legitimate agencies mail documents without postage. IRS correspondence is consistently stamped or postage-paid, indicating private or offshore status.

Clear Line of Authority: Agencies must have a clear delegation of authority; yet, Delegation Order No. 115 indicates the IRS can only audit itself for amounts under $750.

Conclusion: The “Taxpayer” as a Voluntary Status

The ultimate achievement of “Word Magic” is that it requires the individual to “volunteer” into the jurisdiction. In the statutory world, a “Citizen” is a free individual, while a “Taxpayer” is specifically defined as one who collects and submits returns (taxes collected from others) to the federal government. One becomes a “taxpayer” by choice and consent through the signing of forms that are, in reality, affidavits of status.

How to Identify “Word Magic” in Legal Documents

Analyze the Definitions: Locate the “Definitions” section of any code (e.g., 26 CFR 31.3121). If the definition says “State includes Guam,” it means it excludes the fifty states of the Union.

Scrutinize the Casing: Pay strict attention to the capitalization of “United States” and “Citizen.” A lowercase “u” in “united States” points to the republic; a capital “U” points to the federal corporation.

Verify the Master File: Check the Individual Master File (IMF) for “Tax Class 6.” This code indicates the government has classified the individual as having violated laws relating to alcohol, tobacco, or firearms in Puerto Rico, thereby placing them under the enforcement jurisdiction of the Criminal Investigation Division.

Key Takeaway

In the legal realm, you are not what you think you are; you are what you define yourself to be. By failing to grasp the linguistic distinctions between the “united States” (the Union) and the “United States” (the federal zone), a Citizen inadvertently volunteers to become a “U.S. citizen” and a “taxpayer,” accepting a foreign jurisdiction that possesses no constitutional authority over a freeman.

More by Bill Cooper

Bill Cooper Resources Page: https://docs.urbanodyssey.xyz/main/bill-cooper.html

Asset Protection Notes: https://docs.urbanodyssey.xyz/ucc/asset-protection.html

https://theofficialurban.substack.com/p/hott-psych-warfare?r=3kr5wz

https://theofficialurban.substack.com/p/bill-cooper-alex-jones

https://theofficialurban.substack.com/p/bill-cooper-john-lear-1993

https://theofficialurban.substack.com/p/bill-cooper-rare-lecture

Spotify Playlists

Also available on other podcast players, Spotify is the only one that allows me to organize them into playlists and embed them into Substack. See soundcloud link below.

Bill Cooper’s Material (Audio & Writings)

Audio Podcast Episodes (Courtesy of DM Hutchins Research Library): https://mega.nz/folder/IPECUKwT#s9gna8oyLGX1yfZdfCnsgA/folder/VGcWmBRL

Authored by Bill Cooper: https://drive.google.com/drive/folders/12Q1NkAEEkimrp7zkTrJ4_3V_zN5hVdWh?usp=drive_link

Soundcloud Episodes of “The Hour of the Time:” https://soundcloud.com/hour-of-the-time